Why Real Yields Matter More Than the Fed Funds Rate

If you’re watching the Fed funds rate, you’re watching the wrong variable.

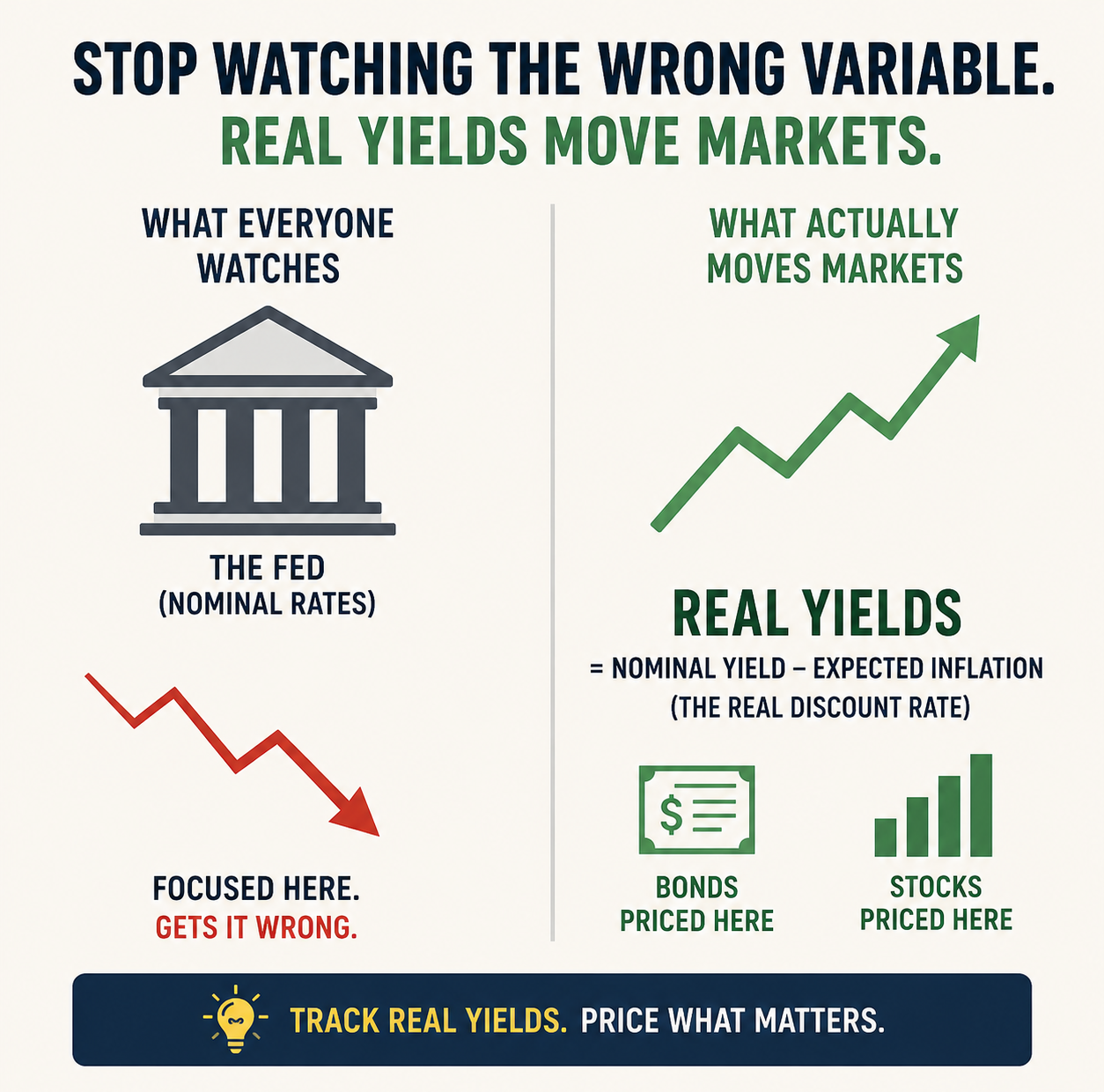

Markets don’t price off nominal rates.

They price off: Real yields.

Defined by the Federal Reserve (FRED):

Real yield = nominal yield – expected inflation

(DFII10 – T10YIE)

This is the actual discount rate.

Why it matters:

When real yields rise:

• Bonds fall (duration compression)

• Stocks fall (valuation compression)

2022 showed this clearly.

IMF + BIS research:

→ Inflation shocks increase real yield volatility

→ Cross-asset correlation rises

Same pattern again.

Implication:

Tracking Fed policy ≠ tracking markets.

Real yields drive pricing across asset classes.

Question: If your model doesn’t explicitly track real yields… what is it actually measuring?